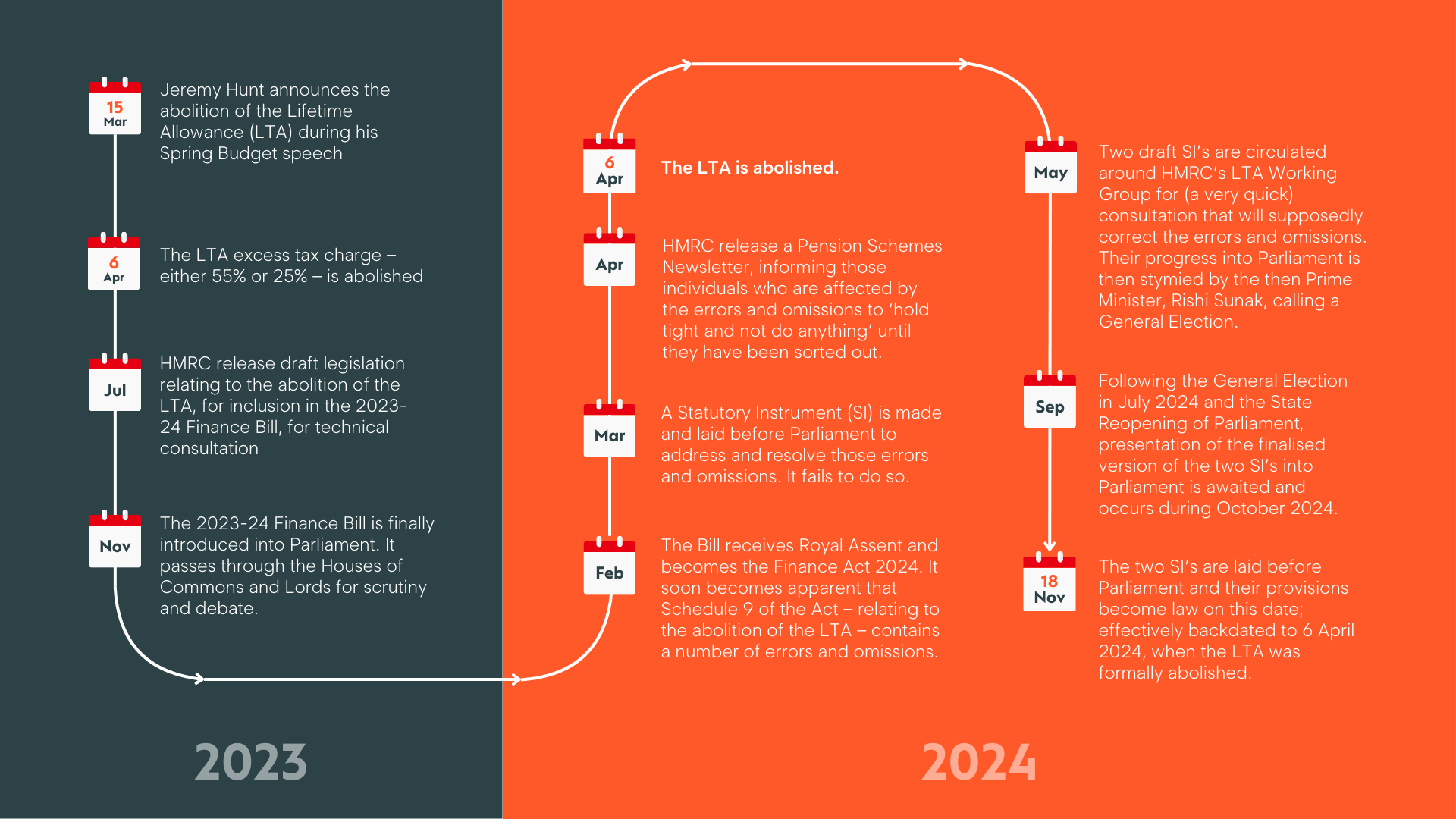

For our very first online Assembly of 2025, we asked whether we’d absolutely definitely seen the back of all the corrective legislation, clear-as-mud HMRC guidance, and lifetime allowance (LTA) limbo that paraplanners, advisers and clients endured for long periods over the previous two years.

So for those who wanted to be certain where things stood, and confirm for themselves that the LTA saga was absolutely definitely over, James Jones-Tinsley from Barnett Waddingham and Transact’s Brian Radbone joined us to put us all straight – once and for all.

Over the course of one lunch hour, James and Brian offered their insights on all the corrections, clarifications and considerations that you could possibly want to know when it comes to the lifetime allowance.

Paraplanners came armed with their questions and comments to share in the chat, and tuned in to hear what our experts – and paraplanners just like them – learned from the saga of the LTA abolition.

A couple of post-event answers

During the event, Colin Stewart of The Paraplanners posed the following question in the chat: ‘If you apply for a transitional tax-free amount certificates (TTFAC), and then fixed protection, can you have the TTFAC recalculated?’. Brian said he’d check and here’s what he found out following the event:

- HMRC’s Newsletter 165 (December 2024) stated that ‘A TTFAC should be cancelled only where the available Lump Sum Allowance (LSA) or the Lump Sum Death Benefit Allowance (LSDBA) is incorrect’. So, if someone obtains FP/IP16 before the deadline and already has a TTFAC, the certificate will become incorrect and must be cancelled. The individual can then reapply with the now correct information.

- It is not possible to withdraw an application either before or after a certificate is issued.

Here’s the relevant bit of the Assembly via Vimeo and Acast if you’re interested in tuning in to the conversation.

{kind=link}